Q2 2025 was a defining period for the global venture capital ecosystem, marked by the unprecedented power of artificial intelligence, a stark bifurcation between capital-rich and capital-poor sectors, and intensified selectivity from investors. Although global VC funding showed resilience, the market’s underlying structure shifted dramatically, with AI mega-rounds skewing totals and traditional sectors facing mounting challenges. This article unpacks the major funding trends, sector and geographic developments, exit environment, and the evolving dynamics shaping the industry's future.

Funding Volumes: Big Numbers, Fewer Winners

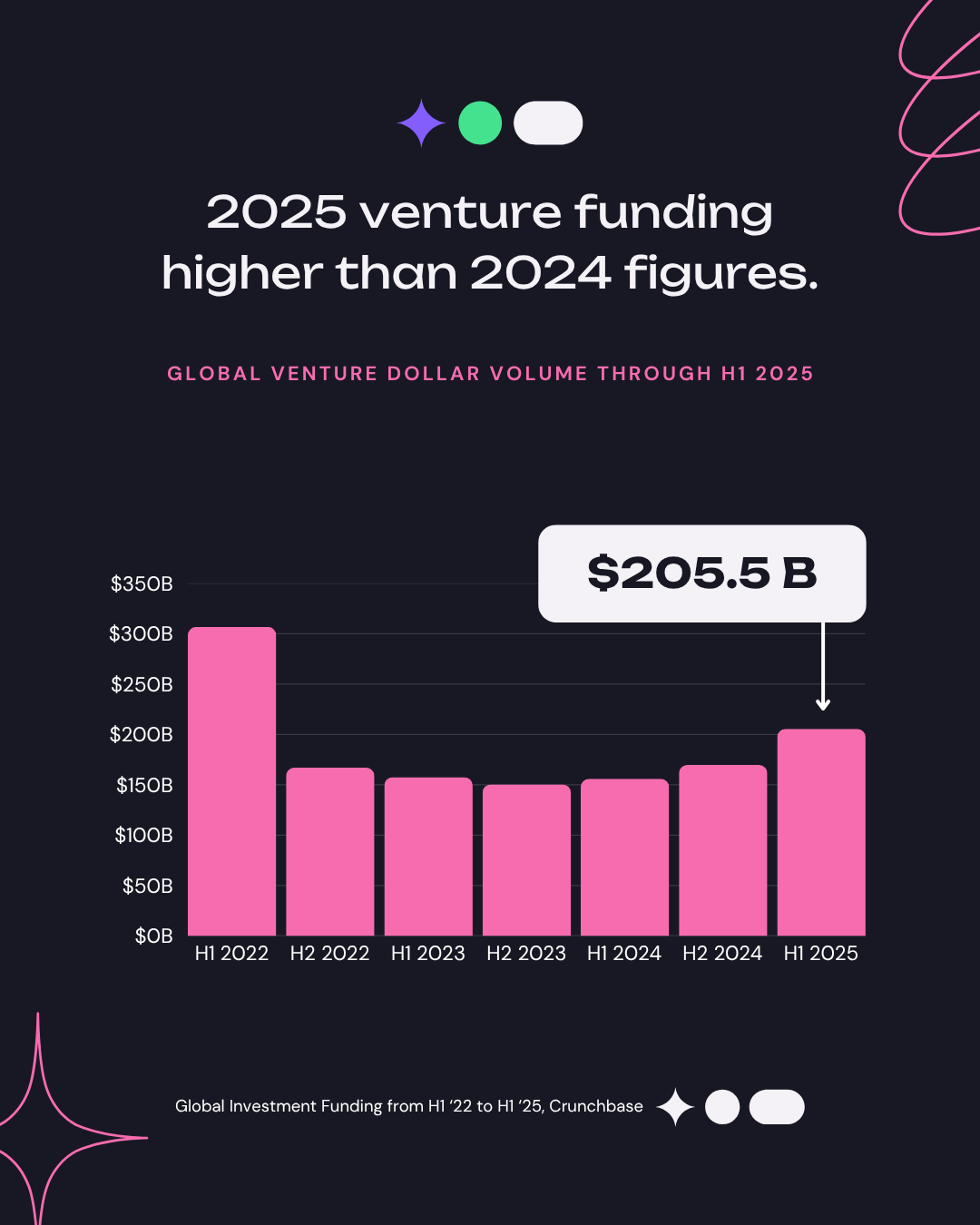

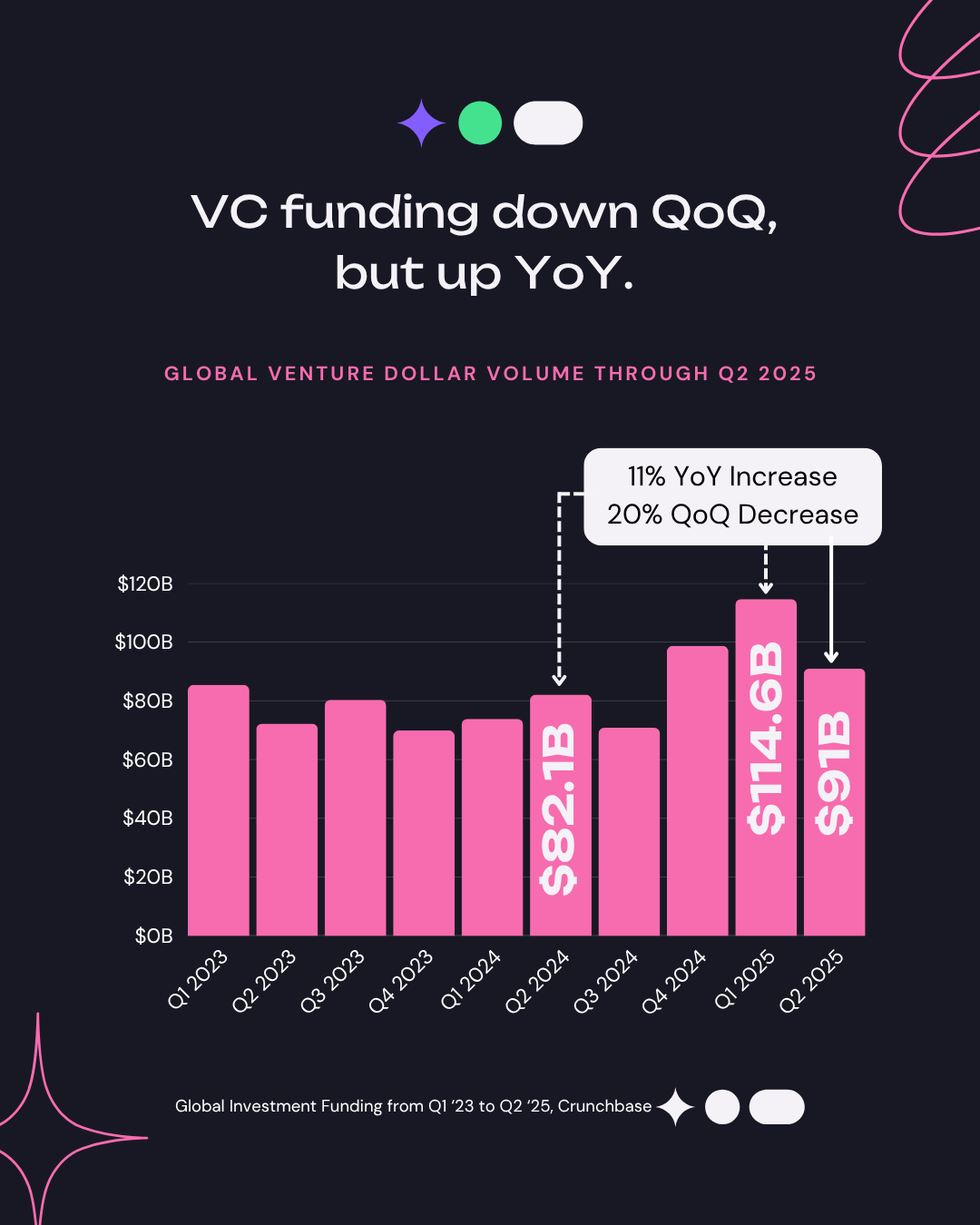

Global venture capital investment reached $91 billion in Q2 2025. While this was an 11% increase year-over-year, it appeared as a sequential 20% drop from Q1’s record-setting $114 billion, which was supercharged by mega AI rounds like OpenAI’s $40 billion raise. The number of completed global deals fell further, continuing a multi-quarter contraction — with just 7,551 deals closed in Q2, compared to almost 9,800 a year prior.

What’s driving the disparity between total dollars and deal count? In short: mega-rounds. Sixteen funding rounds over $500 million accounted for roughly 30% of Q2 capital, translating into oversized influence on headline statistics and a tough environment for early- and mid-stage startups.

The AI Effect: Winner Takes All

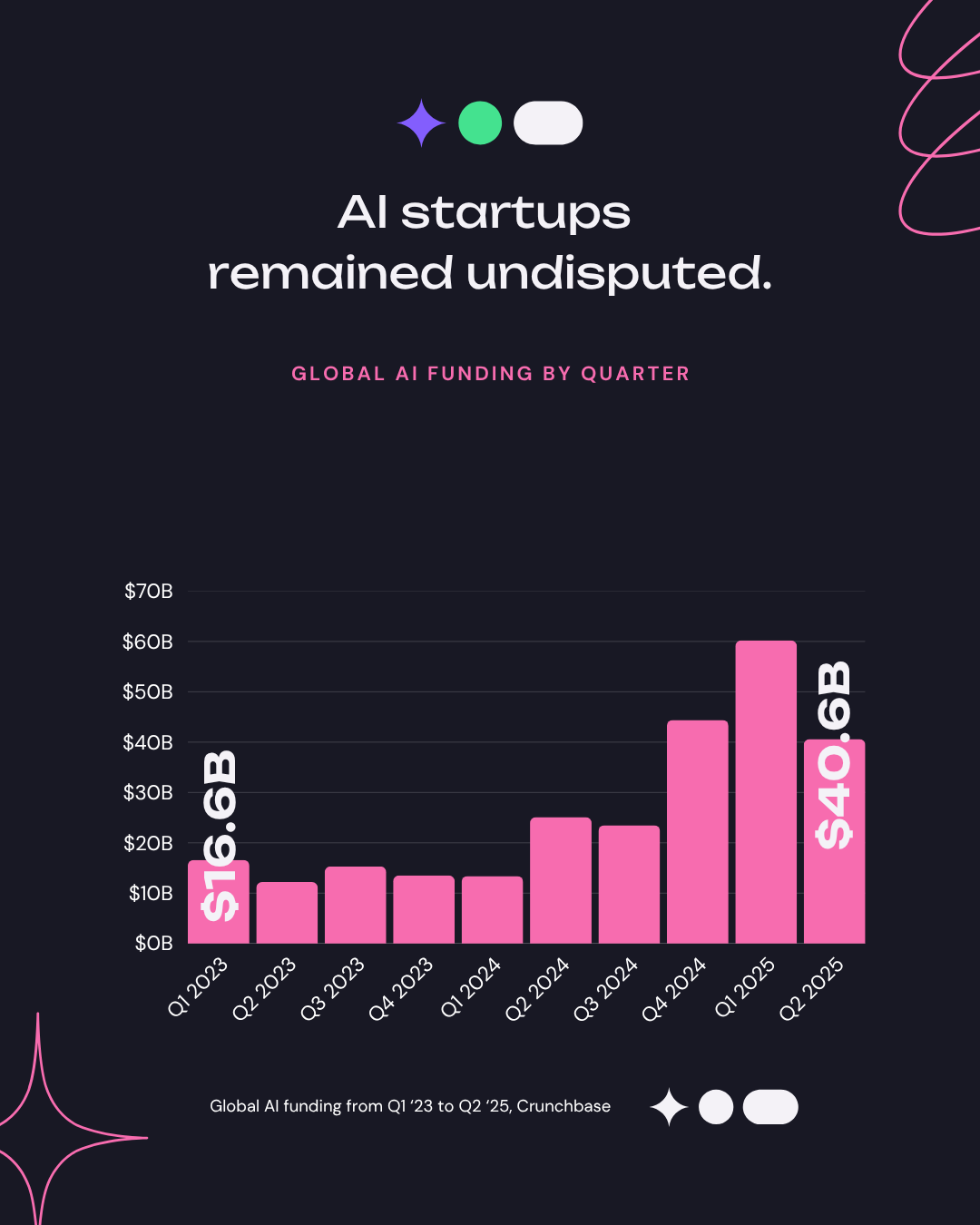

Artificial intelligence was the undisputed centerpiece, capturing a staggering 53% of all VC dollars ($40 billion) in H1 2025. This means that more than half the global capital deployment flowed to AI or AI-powered companies—a dynamic without historical precedent. AI’s gravitational pull was visible in both deal size and sector composition, as the top five funding rounds globally were all AI-related.

Key mega-rounds included:

- Meta’s $14.3B investment in Scale AI

- Anduril’s $2.5B raise (defense & AI)

- Figure AI ($1.5B) and Perplexity ($510M), both advancing sector-specific AI applications

Beyond foundational models, investors targeted verticals including healthcare, legal, defense, and manufacturing—evidencing AI’s shift from hype to industry-embedded reality.

Geographic Distribution: U.S. Strength Centers the Market

North America captured $60 billion—two-thirds of global VC—anchored by U.S. AI dominance. The U.S. registered $145 billion in funding for H1 2025, a 43% year-over-year jump, with most capital flowing to AI, SaaS, and fintech startups. Deal activity, however, continues to drop—demonstrating rising bar for investment and a “flight to quality” ethos.

Europe remained stable with $18 billion in Q2 deployments. Sectors like biotech and crypto saw the most activity, typified by billion-dollar rounds in Binance’s crypto infrastructure and traditional European strengths like enterprise software.

Asia-Pacific hit a new low, down to $12.9 billion in the quarter, as Singapore’s DayOne ($1.2B) was the bright spot amid geopolitical and regulatory headwinds, especially in China. Declines in China were driven by ongoing tensions, data sovereignty issues, and cautious foreign capital.

Sector Trends: AI, Healthcare, and Crypto Compete for the Spotlight

Artificial Intelligence

AI captured not just investment but also boardroom focus. Notably, 58% of North American Series B+ capital went to AI alone. Funding supported both horizontal platforms and vertical-specific solutions, highlighting investor conviction that AI will define the next era of productivity across industries.

Healthcare & Biotech

Healthcare and biotech held second place with $14.8B globally, though biotech in particular has been reset—92% below its 2018 peak. Specialist funds now control 72% of biotech VC, indicating sharpening focus on technical due diligence and exit potential.

Fintech & Crypto

Despite headwinds, fintech attracted $10.8B in Q2, largely due to AI-first startups modernizing infrastructure. Crypto’s resurgence was notable—$10B raised, the highest since early 2022—propelled by stablecoin adoption, tech innovation, and a blockbuster Circle IPO.

Defense/Energy/Industrial Tech

Defense deals commanded attention; Anduril’s $2.5B round led a group of emerging national security and infrastructure companies. The energy transition prompted several mega-rounds, with valuations rarely dropping below prior levels as investor appetite for hard tech rebounded.

Exit Environment: IPOs Roar Back

After two quiet years, the IPO window finally reopened in Q2 2025. VC-backed exits totaled $67.7B, the best since 2021, with Circle Internet Group’s $1.1B IPO delivering a record-breaking stock pop (147% in two days). VC-backed IPOs vastly outperformed PE-backed ones (450% vs. 18% average return), showcasing tech’s public market resurgence. Secondary sales surged: 21% of trades now occur at a premium to last private valuation, up from 13% last quarter.

Unicorn Creation and Valuation Climate

Only eight startups crossed the billion-dollar threshold in Q2, a sharp drop versus the “unicorn glut” of prior years. AI and defense companies (Gecko Robotics, CHAOS Industries, Pathos) dominated, with all but one unicorn emerging from the U.S. Median late-stage valuations continued their slide, reflecting cautious growth projections and widespread down-rounds—now representing one of every five deals for late-stage companies.

VC Fundraising and LP Activity: A Bottleneck Builds

The fundraising environment remains tight for emerging VC managers. 81% of new capital still flows to established funds. LPs show a clear preference for distributions (DPI) over new commitments, with many dialing up co-investment activity (now 88% plan to participate). Europe fared poorly: just €2.3B raised in Q1, projected to be the weakest year since 2015 unless large closes occur late.

What Lies Ahead

The rest of 2025 will amplify current themes: AI’s centrality (even as funding rates cool), a consolidating VC landscape favoring large funds and proven founders, and the slow rebalance in biotech and fintech. With global uncertainties and selectivity on the rise, startups will need clear market fit, strong AI narratives, and operational discipline to raise capital. As the IPO market thaws, late-stage companies sense new urgency to chase a listing or strategic exit while conditions are favorable.

Sources

- https://news.crunchbase.com/venture/global-funding-climbs-q2-2025-ai-ma-data/

- https://angelspartners.com/blog/the-state-of-the-venture-capital-market-in-q2-2025

- https://news.crunchbase.com/venture/na-funding-q2-2025-ai-ipo-ma-data/

- https://www.axios.com/2025/07/03/ai-startups-vc-investments

- https://fortune.com/2025/07/08/q2-venture-funding-climbs-on-ai-deals-while-pe-stuck-on-sidelines

- https://kpmg.com/xx/en/media/press-releases/2025/04/global-vc-investment-rises-in-q1-25.html

- https://forgeglobal.com/insights/startup-trends-top-5-funding-rounds-of-q2-2025/

- https://www.linkedin.com/posts/toddcbertsch_biotechvc-venturecapital-pitchbook-activity-7335312882319949824-Zle1

- https://www.fiercehealthcare.com/health-tech/healthcare-ai-rakes-nearly-4b-vc-funding-buoying-digital-health-market-2025

- https://www.linkedin.com/pulse/ai-first-fintech-leads-way-q2-2025-wealthtech-regtech-kyprianidou-ihttf

- https://cointelegraph.com/news/crypto-vc-funding-q2-2025-surge

- https://blog.equityzen.com/secondary-spotlight-private-company-investment-trends-q2-2025

- https://x.com/twistartups/status/1942377387653476442

- https://ionanalytics.com/insights/mergermarket/ipo-market-shifts-in-2025-as-venture-capital-outperforms-private-equity-ecm-pulse-north-america/

- https://www.forbes.com/sites/marenbannon/2024/11/26/lp-predictions-for-venture-capital-in-2025/

- https://seedblink.com/blog/2025-04-14-state-of-fundraising-in-q1-2025-key-findings-from-market-reports

- https://www.adamsstreetpartners.com/insights/2025-global-investor-survey/